Driving in Bali, Indonesia. Photo credit: Harsimran Julka.

When Uber launched in Indonesia in 2014, the vast majority of the country’s 260 million people couldn’t use it. Credit card ownership isn’t common in the country, and payment by credit card was the app’s only option.

Uber’s magic depends on it: You add your credit card number once and never worry about payment again. Everything happens in the background.

To serve more Indonesian customers, the ride-hailing firm had to sacrifice some of its dearly-held user experience and had to learn to handle cash.

Indonesia, like many developing countries, lacks established cashless payment methods and that’s a major hurdle to digital economy growth.

It’s not just credit cards. Per World Bank’s 2014 data, the majority of the adult population didn’t even have bank accounts.

For the digital economy to reach its expected US$130 billion target by 2020, it needs a breakthrough in cashless payments.

Now, government agencies, banks, telcos, and fintech startups are scrambling to lead the shift away from cash.

There are two main scenarios: one involves the formal banking sector casting a much wider net, dramatically increasing the number of bank accounts, debit, and credit cards in use. In the US, for example, credit cards are a ubiquitous form of cashless payment. According to Statista, there are over a billion credit cards in circulation there. That’s for a population of around 320 million people.

Indonesia’s Central Bank (BI) counts roughly 17 million credit cards in a country of around 260 million people.

It looks a bit better when it comes to debit cards – 143 million are in circulation according to BI. Most of these cards can’t be used for online shopping, and there are only about one million card readers (EDCs) across Indonesia, which means that debit card owners often can’t use them when they want to.

Photo credit: Eko Susanto.

The other scenario looks toward China, where third-party payment providers like Alipay and Tencent Pay have seemingly all but replaced cash overnight.

This was made possible because of the smartphone boom. Credit stored on mobile wallets can be transferred instantaneously and at low cost. In China, the ecosystem of mobile payments has branched out to the point that you use your WeChat app to pay whether you’re at the restaurant or a traditional market.

With regard to mobile phone adoption, Indonesia has done well: 91 percent of the population now own a mobile phone, 47 percent of those are smartphones.

With a payments-ready phone within everyone’s reach, Indonesia might leapfrog card-based payments altogether, some analysts believe. Macquarie Research, the intelligence arm of global financial consultancy Macquarie, suggests this as a possible outcome in its recent Indonesia fintech report. KPMG, which has also created a substantial report on payments in Indonesia, comes to a similar conclusion.

The scenarios aren’t mutually exclusive – traditional bank payments and alternative forms of e-payments can co-exist. Both depend on the technical innovation and agility brought about by fintech startups.

But at this point, no one can say how the shift from cash will play out in Indonesia – and which businesses and institutions will reap the largest rewards.

The state of pay

So how do people pay for things in Indonesia?

In traditional offline retail, there’s little choice but to pay in cash. Shops in malls, restaurant chains, or hotels have card terminals, but once you’re outside of established retail, that option no longer exists.

To settle bills like electricity, water, or internet, Indonesians use ATMs, online banking, or pay in cash through agents, for example at convenience stores.

Convenience stores let customers pay bills and buy digital vouchers at the counter. Photo credit: Tech in Asia.

For payments in digital environments, there’s no obvious solution. Shoppers are smothered with choice.

Screens with an overwhelming amount of payment options – here from popular shopping site Tokopedia – are common during the checkout process.

Screenshots from Tokopedia app.

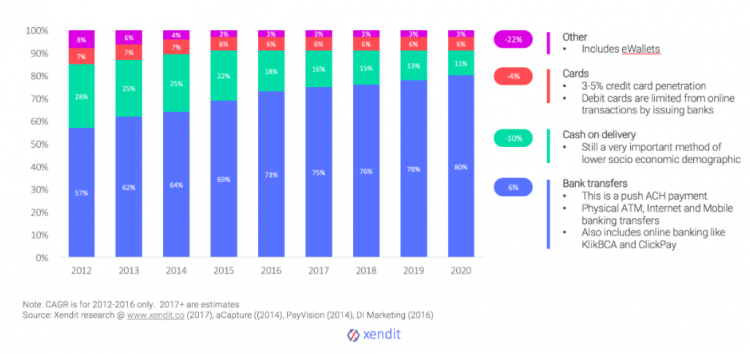

The most common methods to settle online payments are ATM transfers and online banking, followed by cash-on-delivery (COD) – when you pay in cash through the delivery person.

The Indonesian Association of Internet Providers (APJII) and Xendit, a payment gateway, both come to this conclusions in their research.

Chart: Xendit.

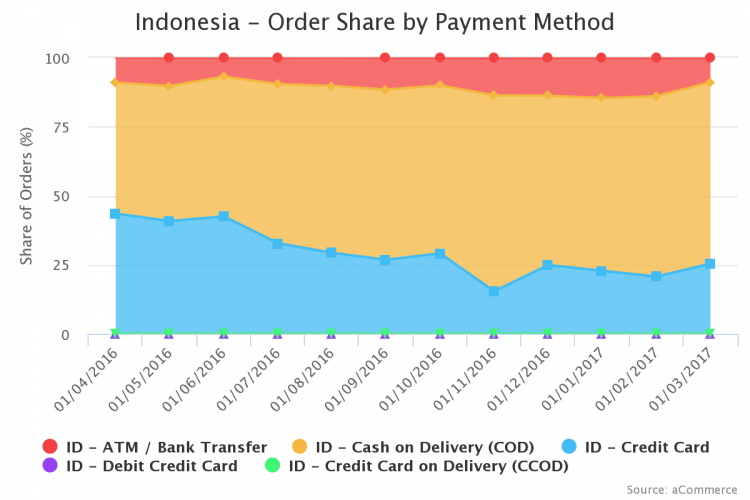

A slightly different view is presented by eCommerce IQ in its analysis of data from ecommerce enabler aCommerce.

Chart: EcommerceiQ.

It sees an overwhelming demand for COD, with ATM payments coming in second. That’s because the data was collected mainly from e-retailers that send out physical goods, aCommerce IQ told Tech in Asia. This skews results in favor of COD.

Xendit and APJII’s research includes people’s preferences when paying bills and digital goods like tickets and gaming vouchers.

Consumers may have arranged themselves with ATM transfers, online banking, and COD payments, but these methods have obvious disadvantages.

It’s risky for businesses to trust a delivery person with cash. It also adds to cost of transactions, delays in settlements, and more returns or undelivered items. ATM payments and online payments are a hassle for customers, and they’re also not instantaneous. Overall, this friction leads to many unsettled payments. Industry players speak of a 80 percent card abandonment rate.

In 2017, card payments and other forms of cashless payments, such as through mobile wallets, only account for a small fraction of overall payments in Indonesia – even though they promise a smoother experience.

In part two, we’ll explore how Indonesia’s formal banking sector is adapting to change.

This post Indonesia’s long road to cashless payments appeared first on Tech in Asia.

from Tech in Asia https://www.techinasia.com/indonesias-long-road-to-cashless-payments-pt1

via IFTTT

No comments:

Post a Comment