Photo credit: Pixabay.

India is routinely touted as the world’s third biggest startup ecosystem, the fastest growing one, the third best funded one, and so on. But there’s a vital cog missing: exits of substance, which cross US$5 million in value.

Taken as a whole, the number of exits and even their aggregate value surged in 2015 and there’s been no let-up this year. The devil is in the details.

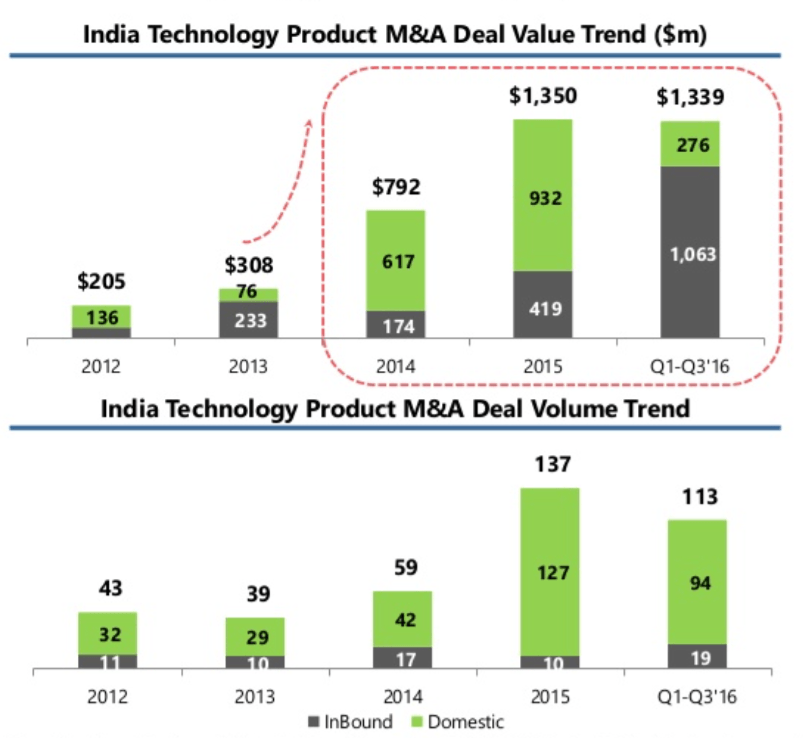

Last year, there were 135 M&A (mergers and acquisitions) deals in the tech product space – 130 percent more than in 2014 – and the total value of these deals was US$1.35 billion (70 percent more than in 2014), points out a study by tech industry think tank iSPIRT and strategic advisory firm Signal Hill.

The momentum has continued in the first three quarters of this year: there have already been 113 M&A deals and the number is likely to cross that of 2015. As for total deal value, it’s likely to surpass last year’s US$1.35 billion substantially because US$1.34 billion got notched up in the first three quarters of 2016.

But a closer examination reveals the missing cog.

The missing link

What’s striking in the chart above is that 94 out of the 113 deals this year were domestic, but they constituted only a little over 20 percent of the total deal value. It’s the inbound deals which tend to be substantial, but there were only 19 of them.

Three-quarters of the deal value since 2014 came from just eight deals.

Two-thirds of the US$1.34 billion M&A value in Q1-Q3 this year came from a single deal: the US$900 million buyout of Div Turakhia’s Media.net by a Chinese consortium, one of the biggest cross-border adtech acquisitions.

Overall, nearly three-quarters of the deal value since 2014 came from just eight deals. So they hide the low volume of substantial exits in the ecosystem as a whole.

Most of the big ones represented industry consolidation:

- CarTrade buying Carwale for US$88 million

- Quikr buying CommonFloor for US$120 million

- Payu buying CitrusPay for US$130 million

- Ola buying TaxiForSure for US$200 million

- Flipkart buying Myntra for US$370 million

The others were for strategic product or market access, such as:

- Snapdeal buying FreeCharge for US$400 million

- Wirecard buying GI Retail for US$372 million

- The Miteno-Media.net US$900 million deal

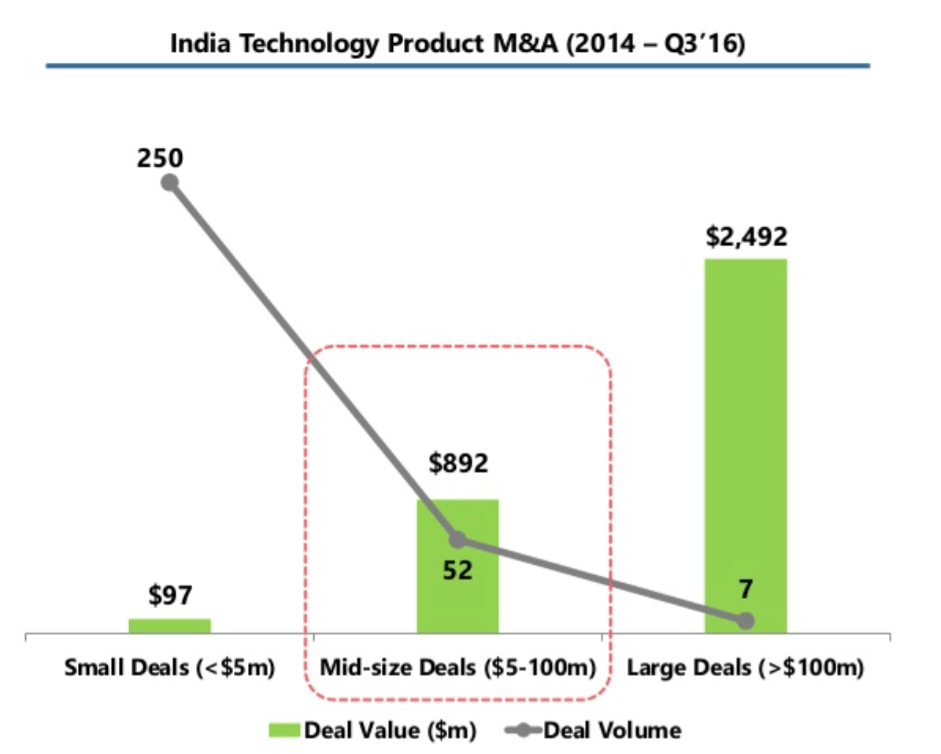

The bulk of the exits – 80 percent of them – were tiny pops. As many as 250 M&A deals out of the 309 from 2014 to Q3 of 2016 had a value below US$5 million. They accounted for less than US$100 million collectively in transaction value, yielding an average deal size of less than US$400,000. The 250 deals together were worth less than what Quikr paid to buy CommonFloor (in stock) or less than a quarter of Snapdeal’s acquisition of FreeCharge.

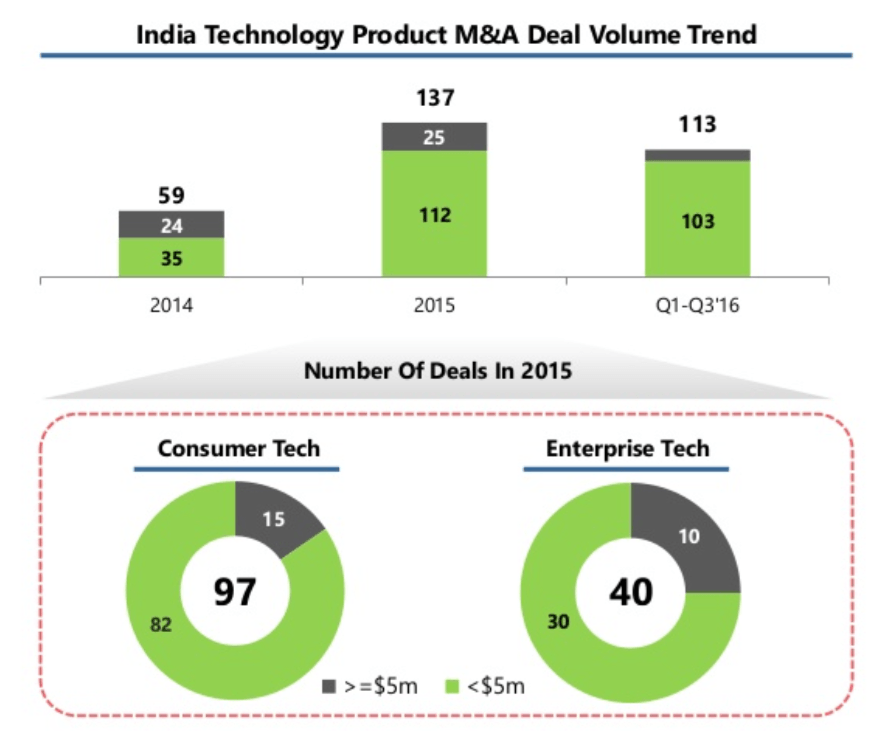

What the iSPIRT-Signal Hill analysis shows is an uptick in mega deals – seven out of the eight big acquisitions happened over the past couple of years, with only the Flipkart-Myntra deal being from 2014. There’s also been a plethora of small pops, with the sub-US$5 million deals surging in 2015 and this year.

What’s missing is the middle layer – M&A deals of substance in the US$5-100 million range. Only 52 of the 309 deals from 2014 to Q3 in 2016 – about one-sixth of the total – fell in that range. The total transaction value of these deals – US$892 million – gives an average deal value of US$17 million. That’s a decent average, but there are just too few of them.

See: A ranking of 151 enterprise-ready startups from India

Transition period

The mid-size deals are important because they increase the chances of VCs getting returns on their investment. The deals below US$5 million are mostly write-downs or acqui-hires of bootstrapped or seed-funded startups struggling to raise follow-up funding. So it’s only the 60 deals above US$5 million in value which have given some returns – and even among them, there are major write-downs like Rocket Internet’s fashion portal Jabong selling for a song to Flipkart. A company once reportedly valued at US$1.2 billion was sold for a mere US$70 million.

The average size of 80 percent of M&A deals since 2014 is a mere US$400,000.

One can argue that it’s still early days for the ecosystem because major fund flows picked up only in 2014 when over US$5 billion got invested. It rose even higher in the India fixation of 2015. This year has been a time of reckoning, with more attention being paid to unit economics and a path to profitability than to a market grab.

That is why there has been a shift in focus to B2B (business-to-business) startups and enterprise tech in the interim period, while the jury is still out on sustainable business models for startups targeting the fast-growing internet and mobile consumer market. A quarter of the M&A deals in enterprise tech were above the US$5 million mark in 2015, whereas less than 15 percent of the deals in consumer tech were above that mark.

Investor interest in India remains high despite the lopsided exit scenario. The latest cases in point are Accel Partners raising US$450 million for its fifth India fund and SoftBank chairman Masayoshi Son stating his intent to top the US$10 billion investment he had committed for India.

Investors know that it may take a few more years for startups funded in the boom years of 2014 and 2015 to mature for substantial exits. But exits of US$5 million and above, as well as tech IPOs, will have to pick up eventually for India to remain a hot destination for VCs and private equity (VC/PE), which fuel the bulk of startup innovation and growth in the country.

See: 45 hot software product startups from India and their cool ideas

Sucker deals

One of the biggest disappointments has been the inability of the early consumer internet and ecommerce companies to provide exits for their investors – except by sucker deals of selling their stakes to the next investor at a hyped-up valuation. The last one in the line is left holding the can, as we’re seeing with SoftBank’s recent write-down of its investments in ecommerce marketplace Snapdeal and ride-hailing app Ola.

A healthier exit scene is vital to sustain the momentum India’s startup scene has gained in the last three years.

A flight of venture capital may seem far-fetched in an ecosystem with as much potential to grow as India. But some appear to have already fallen out of love with India – Tiger Global, one of the biggest investors of the 2014-2015 boom years, made just three investments this year. There has been a rise in failures along with the fall in funding in this corrective phase.

A healthier exit scene is vital to sustain the momentum India has gained in the last few years and turn the doubters into believers. A comparison with Silicon Valley shows how far behind India is in achieving that.

See: Something’s rotten in India’s startup scene – and it’s time to call it out

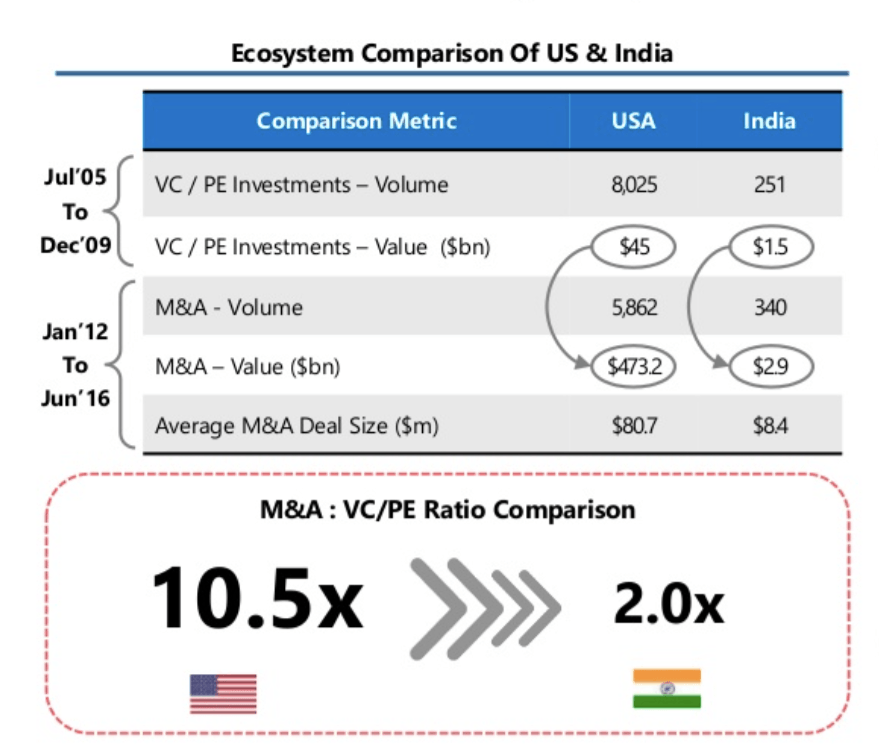

Between July 2005 and December 2009, the US saw US$45 billion in VC/PE investments in tech startups. And between January 2012 and June 2016, tech M&A amounted to US$473 billion. That suggests an overall exit value of 10x over the

capital invested.

The comparative figures for India were US$1.5 billion and US$2.9 billion, for a capital exit ratio of less than 2x. The ratio needs to reach at least 4x for the VC-powered tech startup ecosystem to start humming. Until then, it rides on hope.

This post https://www.techinasia.com/indian-startups-eat-only-paper-profits appeared first on Tech in Asia.

from Tech in Asia https://www.techinasia.com/indian-startups-eat-only-paper-profits

via IFTTT

No comments:

Post a Comment